Dr.-Ing. Kai Steffens

Managing director BDO Technik- und Umweltconsulting GmbH

Research and development are key drivers of progress for companies – but they require not only technical expertise, but also strategic financing. The tax incentive for R&D provides companies in Germany with an attractive instrument for sustainably promoting innovation projects. Unlike traditional subsidies, companies benefit from a comparatively uncomplicated application process that can also be used retroactively. Whether in-house or as part of collaborations or contract research, tax incentives for R&D can be applied not only for future projects, but also for ongoing and already completed projects. Even companies in loss-making phases benefit directly from a payout.

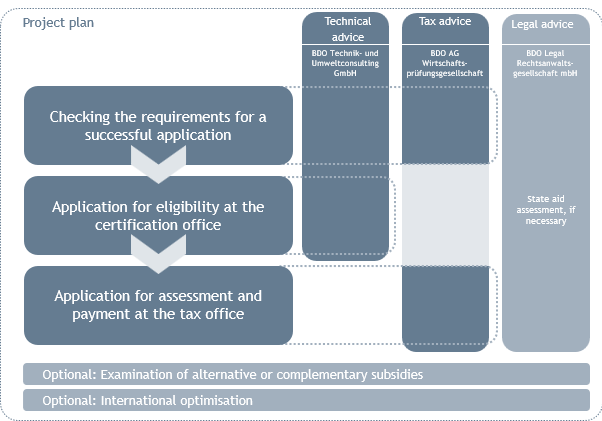

We accompany you throughout the entire process: from project evaluation and application to optimal tax structuring – in an interdisciplinary, efficient and solution-oriented manner.

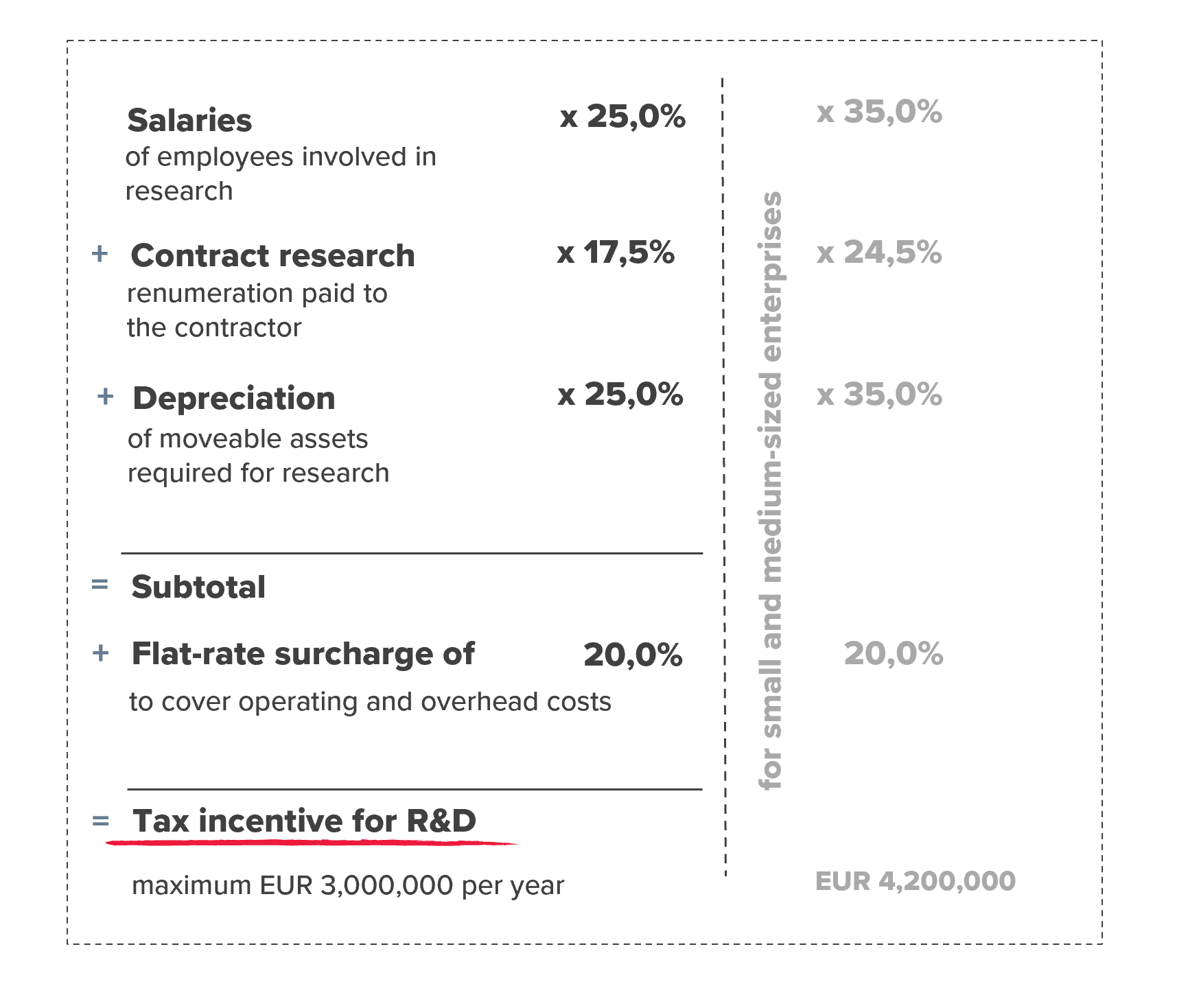

With an annual funding amount of up to EUR 3,000,000 or EUR 4,200,000 for small and medium-sized companies, the tax incentives for R&D are an interesting instrument for financially optimizing own or commissioned research and development projects and reducing the tax burden.

In addition to the wages of the researching employees, the expenses incurred within the scope of the contract research and the depreciation of the movable fixed assets required for the research are eligible. For research and development projects starting after 31st December 2025, a flat-rate surcharge of 20% will also be considered to cover operating and overhead costs incurred.

The tax incentives for R&D reduce the income tax burden in the next tax assessment. Any remaining surpluses are not carried forward but refunded directly. This means that companies can benefit directly even if the tax incentives for R&D claimed are higher than the current income tax burden.

In addition to an overview of our subsidy consulting services, you will find relevant key points on other topics in this context below:

We are happy to assist you with optimal structuring, checking application requirements, the application process or further questions, whether of a tax, technical or legal nature.

Tax structuring and the application to determine the tax incentives for R&D requires tax expertise. However, this application is only the second step in the research grant application process. In the first step, it is not tax specialists from the tax authorities who check whether a project is eligible for funding, but engineers or scientists from the certification office. At BDO, you receive the necessary advice and support from a single source.

Companies with unlimited and limited tax liability within the meaning of the Income and Corporation Tax Act that meet the other application requirements are eligible. Sole proprietorships, corporations or domestic permanent establishments can therefore benefit from the research allowance. Partnerships are also eligible, with the research allowance being paid out at the level of the partners.

The tax incentives for R&D consider the requirements of the General Block Exemption Regulation (GBER). This is a European Union regulation that allows member states to grant certain groups of state aid without prior approval from the European Commission. Based on these provisions, companies in particular that are in difficulty are excluded from the research allowance. The GBER sets out the binding criteria that must be met in order to qualify as a company in difficulty. An examination on the basis of the GBER is therefore required before an application is submitted. Although the assessment must generally be carried out at the level of the applicant company, the consolidated financial statements are decisive for companies that are fully consolidated within the framework of consolidated financial statements.

As the criteria must be fulfilled for reasons of state aid law at the time of acquisition of the legal entitlement to a research allowance, the economic framework conditions must be examined at the end of each financial year for which an application for tax incentives for R&D is to be submitted.

Research and development projects are eligible for tax relief if they are classified as basic research, industrial research or experimental development. The distinction is also made here based on the definitions of the General Block Exemption Regulation (GBER), which are substantiated by the statements and explanations of the OECD Frascati Manual.

Among other things, a distinction must be made between this and a routine improvement, which does not fall under the scope of research and development and is therefore not covered by the research allowance. In terms of time, the tax incentives for R&D are granted until the product or process is established and from then on, the focus is solely on market development as the primary objective.

Attention should already be paid to the exact project description in the application for eligibility, which in practice is quite a challenge due to the limited length of the text that can be submitted. Relevant experience in formulation is helpful and increases the chances of a successful application.

Below, we provide a brief overview of which projects are eligible for funding and under what conditions. Further information can be found under the respective headline.

The research grant is subject to application. A one-off application for eligibility must be submitted for the respective research and development project and an annual application must be submitted for all research and development projects in the respective financial year to determine the re-search allowance. This is therefore also referred to as a two-stage application procedure.

The application for eligibility of the research and development project must be submitted electronically to the Research Allowance Certification Office (BSFZ). The application must include some key data on the applicant company and describe the research and development projects. However, the presentation is limited in scope, which requires a very brief and concise presentation. Experience in submitting applications is therefore very helpful to sufficiently explain the aspects and critical points relevant to the examination by the certification office.

The certification office checks whether the activities described in the application constitute a project eligible for funding within the meaning of the Research Allowance Act and thus primarily relates to the technical part of the project. If the project is eligible for funding, it issues a certificate that is binding for the tax office.

Based on the certificate, the eligible company can apply for tax incentives for R&D to its tax office after the end of the respective financial year.

The tax incentives for R&D are determined in a separate notice and are fully offset against the tax assessed in the next first income or corporation tax assessment of a year. If the tax incentives for R&D exceed the assessed tax, a refund is made so that companies with a low tax burden as well as companies in loss-making phases also receive direct support. This means that the tax incentives for R&D are also an interesting subsidy for start-ups with start-up losses.

We would be happy to advise you on all tax aspects of the research allowance. The colleagues at BDO Technik & Umwelt Consulting GmbH can also help you with all technical issues and the colleagues at our cooperation partner BDO Legal Rechtsanwaltsgesellschaft mbH can help you with all legal issues such as contract reviews in the context of contract research or state aid law issues.